%201.svg)

Blog

CGO / CMO

Growth Operating System

What Your CFO Is Really Looking For When They Ask About LTV:CAC

David Manela

November 18, 2025

.png)

When a CFO asks for LTV to CAC, they are not asking for a dashboard ratio. They are asking whether your growth engine creates value in a predictable, profitable way. This ratio is only meaningful when the underlying system is understood, trusted and actively managed.

This is the core idea behind David Manela’s approach: LTV is not a metric. It is a system.

Most teams treat it as a slide number. Your CFO wants to know whether it operates as a discipline inside your company.

A CFO’s first question is not “what is our LTV.”

Their real questions are:

If the team cannot answer these, the ratio loses meaning.

The full LTV equation is a system of levers:

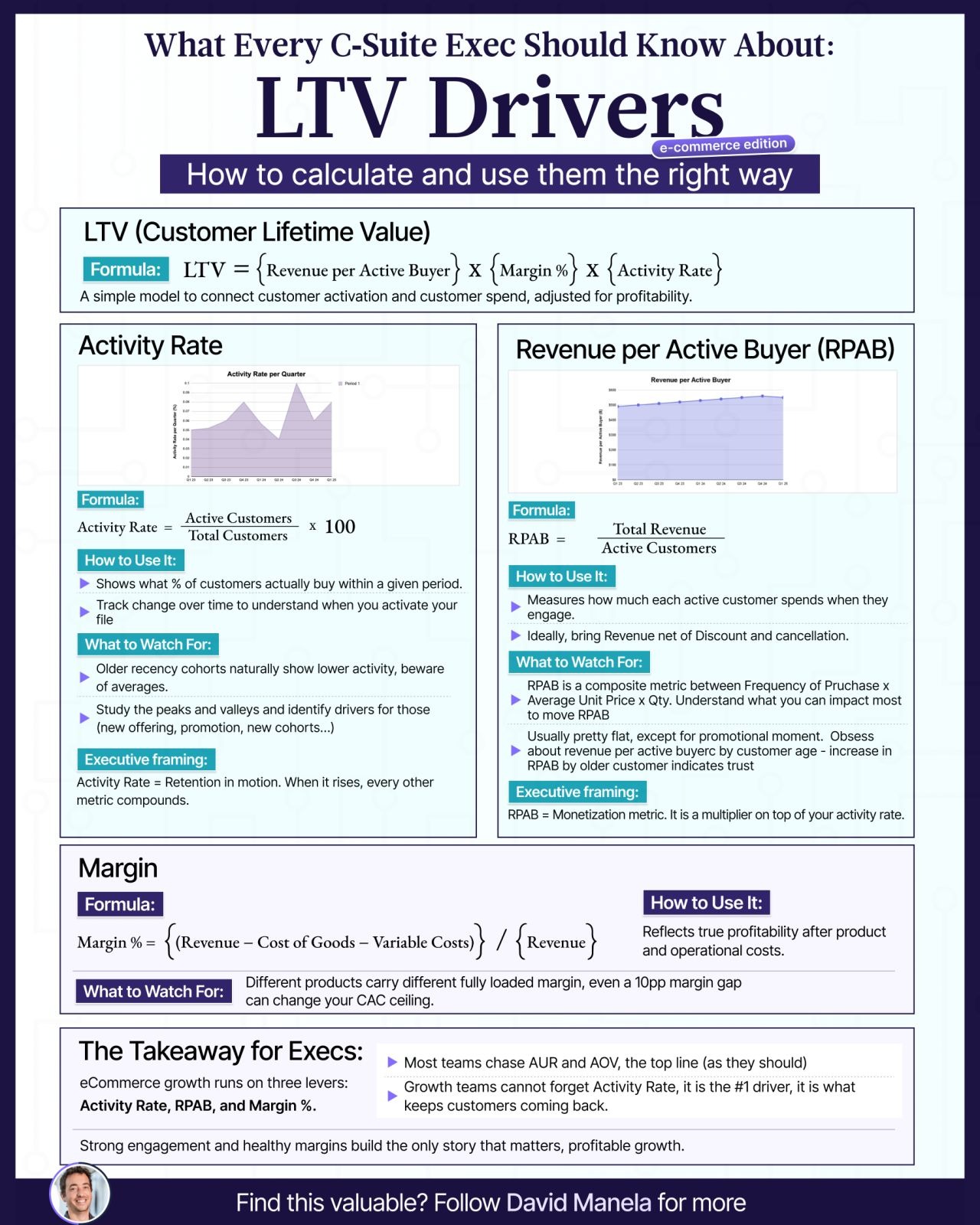

LTV = (Average Unit Price × Items per Order) × Purchase Frequency × Margin Percent × Activity Rate

Most companies over-rotate on AOV and purchase frequency because they are easy to see and easy to report. CFOs look deeper.

Your CFO wants to understand what makes buyers return, how quickly they reactivate and whether their behavior compounds over time. Activity Rate is a leading indicator of retention and lifetime value, and it shows whether marketing and experience are creating durable habits rather than one-off transactions.

To a CFO, LTV means nothing without margin. They want to understand where value is created, where it leaks and how this connects to CAC. A channel may drive volume but destroy profitability. Another may deliver fewer customers but generate high Contribution Margin. Your CFO wants transparency in this tradeoff and clarity on which levers improve the blended margin profile.

Boards want to know whether the business grows through increased frequency, increased spend, better retention or all three. CFOs want to know whether these behaviors hold across cohorts or whether the current LTV is masking decay. This is why they push for consistent definitions and auditable data.

LTV to CAC is not a report. It is a roadmap.

What your CFO truly wants:

Violet blends financial accuracy with growth insights. It tracks the full LTV system, connects it directly to CAC and lets both finance and growth teams see the same truth. This gives CEOs confidence in compounding value, gives CFOs visibility into profitability and gives marketing a clear path from activity to revenue.

When your CFO asks for LTV to CAC, they are asking whether your company can grow in a capital efficient, repeatable way.

When the LTV system is operational, not theoretical, the answer becomes far more compelling.

.png)

.png)

.png)

%201.png)

%201.svg)

%201.png)